Blockchain is a technology that has gained a lot of attention in recent years, and you may have heard the term mentioned in the context of cryptocurrencies like Bitcoin. However, blockchain is much more than just a tool for digital currencies. In simple terms, blockchain is a decentralized and transparent system that allows multiple parties to securely and immutably record and verify transactions without the need for a central authority. Let’s dive deeper into what blockchain is and how it works and it is easy to understand especially for beginners.

Blockchain is a technology that has gained a lot of attention in recent years, and you may have heard the term mentioned in the context of cryptocurrencies like Bitcoin. However, blockchain is much more than just a tool for digital currencies. In simple terms, blockchain is a decentralized and transparent system that allows multiple parties to securely and immutably record and verify transactions without the need for a central authority. Let’s dive deeper into what blockchain is and how it works and it is easy to understand especially for beginners.

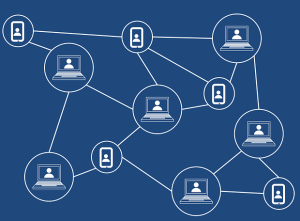

At its core, a blockchain is a digital ledger or a record of transactions. But unlike traditional ledgers that are typically centralized and controlled by a single entity, a blockchain operates in a decentralized manner. Instead of relying on a central authority, blockchain uses a network of computers, often referred to as nodes, to collectively maintain and validate the ledger.

Imagine a spreadsheet that is duplicated thousands of times across a network of computers. Each computer in the network has a copy of the entire spreadsheet, and they all work together to validate and agree on the contents of the spreadsheet. This is the fundamental idea behind blockchain.

One of the key features of blockchain is that it is designed to be secure and tamper-proof. Each transaction recorded on the blockchain is grouped together in a block. Once a block is added to the chain, it becomes very difficult to alter or remove the information within it. This is because each block contains a unique identifier called a hash, which is generated by applying a mathematical algorithm to the data in the block. If any data within the block is changed, the hash would also change, alerting the network that the block has been tampered with.

To maintain the integrity of the blockchain, consensus mechanisms are used. Consensus mechanisms are algorithms that enable the network of computers to agree on the validity of transactions and the order in which they are added to the blockchain. Some popular consensus mechanisms include Proof of Work (PoW) and Proof of Stake (PoS). These mechanisms ensure that all participants in the network follow the same rules and agree on the state of the blockchain.

Blockchain technology has many potential applications beyond cryptocurrencies. For example, it can be used for supply chain management, where every step of a product’s journey is recorded on the blockchain, ensuring transparency and traceability. It can also be used for voting systems to enhance security and prevent fraud. Additionally, blockchain has the potential to revolutionize the financial industry by enabling faster and more secure cross-border transactions and reducing the need for intermediaries.

It’s worth noting that blockchain is still a developing technology, and there are challenges to overcome, such as scalability and energy consumption. However, ongoing research and development efforts are aimed at addressing these issues and unlocking the full potential of blockchain.

In conclusion, blockchain is a decentralized and transparent system that allows multiple parties to securely and immutably record and verify transactions without the need for a central authority. It is designed to be secure, tamper-proof, and relies on consensus mechanisms to ensure the integrity of the ledger. While blockchain has gained prominence through cryptocurrencies, its potential applications extend far beyond digital currencies. As the technology continues to evolve, we can expect to see blockchain being adopted in various industries, transforming the way we conduct business and interact with digital systems.